Protecting shareholder interests – many imperfect solutions

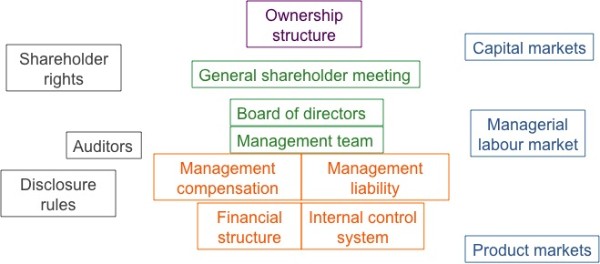

The corporate governance discussion generally focuses on executive remuneration, supervisory boards, shareholder activism and transparency. But in practice there are many more mechanisms capable of constraining the behaviour of top management. The figure below presents the overall institutional set-up that is part of or directly influences the governance of a corporation.

Corporate governance – the overall institutional context

None of these many control mechanisms works perfectly. In practice, they are combined. The best mix depends on many circumstances. Finding it is an art in itself. Theory provides useful hints, but cannot replace personal judgement.

The following list gives an overview of the major control mechanisms, their possible contribution to a solution of the agency problem and their respective shortcomings.

Ownership

Strengthening minority shareholder rights

Dispersed ownership makes best use of the risk diversification and liquidity advantages of stock markets. However, under dispersed ownership shareholders have no interest to actively exercise control over management.

Regulations that make it easier for minority shareholders to exercise their control rights at shareholder meeting or through derivative suits will not improve the dilemma. Small shareholder cannot afford the costs of acquiring enough knowledge and expertise to exercise effective control. Giving small shareholders too much power runs the risk that some will abuse this power to menace and blackmail the corporation.

Controlling shareholders

Owners with a large share have an interest to control management and also sufficient influence.

However, they forego advantages of risk diversification and liquidity. And they may abuse their close contact with management and influence to gain personal advantage, for example through insider trading or the “tunnelling of profits”. This then requires additional regulation and creates new control costs.

Institutional investors

Unlike small shareholders, institutional investors have the expertise and influence to exercise control, but unlike controlling shareholders, they are not strong enough to abuse their influence.

However, they also forego risk diversification and liquidity advantages. And what makes us expect that institutional investors exercise effective control? They are also managing other people’s money. So we encounter here an additional agency problem.

Delegation of control rights

Proxy voting as a solution

Many small shareholders may delegate their control rights to someone with enough expertise to judge the performance of management. Such an agent would then not only have the expertise, but also the voting power to exercise effective control over management.

However, who ensures that such an agent acts in the interest of small shareholders? The delegation of control rights only replicates the agency problem.

Supervisory boards

Board members should be better able to judge the performance of management. They are also granted more formal power over management and have better access to information.

However, who ensures that the right people sit on the board? That they are independent, yet informed enough to exercise control? Who makes sure that independent, well informed directors take their job serious? Again, we basically replicate the agency problem as in the case of proxy voting. Theory has yet to show why the principal agent problem between shareholders and managers can be resolved by introducing a principal agent problem between shareholders and a board of directors.

Transparency – disclosure rules

Strict disclosure rules reduce the information asymmetry between outside investors and management, thus making it easier to evaluate performance and exercise control.

However, we cannot expect companies to disclose all information, because this would harm their competitive position. Where do we draw the line? The more often and the more comprehensive reporting has to be done, the more expensive it becomes. Independent auditors are needed to assess the correctness of the disclosed information. How do we ensure independence, if the auditors are paid by the companies they audit? To interpret such information correctly requires a lot of know-how that only a few experts have.

Incentive pay

Tying the income of managers to their performance should make them exert more effort to achieve a good performance. Incentive pay thus helps to align the interests of managers and shareholders.

However, performance is also influenced by chance factors. Risk averse managers will need to be compensated for the higher risk inherent in performance-based pay. Stock options offer a solution here as they limit the downward risk, but they may then induce management to choose too risky investments.

How do we measure performance? Share prices are not a good measure as they are also influenced by macro-economic and industry wide factors. The share price relative to an industry index captures the performance of a management team more accurately because it contains less “noise”. But such measures are hardly applied. Why?

How do we ensure that managers will not manipulate the measure? If 80 percent or more of a manager’s remuneration depends on performance, the more he or she might seek ways to influence the measure beyond better performance.

Stricter liability

Managers should be made liable if they are not managing company resources carefully enough. They should not be able to fully insure against such liability.

However, managers decide about risky projects in a complex and dynamically changing environment. It is hard to prove that they could have avoided a loss making decision. The more they are made liable, the more risk averse they will become and the more pay they will require.

Control function of stock markets

General considerations

Managers of listed stock companies are monitored by investors, analysts and other market participants. Bad performance will translate into lower stock prices and this might have various disciplining effects, for example by lowering stock price based incentive pay.

However, the information feeding into stock prices tends to be incomplete, can be manipulated by management or market participants and also reflects macro-economic and industry wide factors.

Cost of capital

The power of management is closely linked to the ability to finance new projects. Lower share prices will make it more expensive to raise additional outside capital, thus punishing poor management.

However, the mechanism will not be effective in companies with abundant internal funds.

Hostile takeovers

Bad performance leading to lower share prices may induce takeovers attempts by investors that are confident of being able to manage the resources more productively. To avoid such risks, managers will try to perform well.

The disciplining effect of hostile takeovers is constrained by two major hurdles. Takeover regulations normally require that share holdings are made public and that investors acquiring a certain position reveal their intentions. This will induce competitive bidding for the company, making an acquisition less worthwhile. Incumbent management may also resort to actions to actively prevent a hostile takeover attempt, for example by issuing new shares to dilute the position of the offender.

The managerial labour market as a control mechanism

Should managers not be disciplined enough by the threat of losing their job if they perform bad, especially if such bad performance lowers their chance to find an equally well paid job at another company?

The disciplining effect of an outside labour market should not be underestimated. However, it confronts the same information asymmetries as a stock market.

Longer-term career concerns should impose an even stronger disciplining effect than income losses. However, this holds only true for managers with a sufficient number of years of service ahead of them.

Reducing free cash flow

The ability of managers to misuse corporate funds is closely linked to the amount of free cash flow at their disposal. Reducing free cash-flow should thus alleviate the governance problem.

Higher leverage

A higher ratio of debt to capital will channel earnings into interest payments, thus reducing the cash flow at the disposable of management.

However, a higher leverage translates into a higher risk and higher costs of financial distress.

Competition in product markets

Free cash flow will also be reduced if markets are sufficiently competitive so that profits are moderate and bad management is quickly revealed through losses in market shares and revenues. Such a solution to the governance problem might not be welcome by shareholders, but it would be in the general interest of society.

The disciplining effect of competition is probable one of the major governance mechanisms a market economy can provide, even though few markets fulfil the structural requirements of perfect competition.

And more …

The list could be further extended – internal control systems, investor relations, public regulation, but the imperfections would remain.