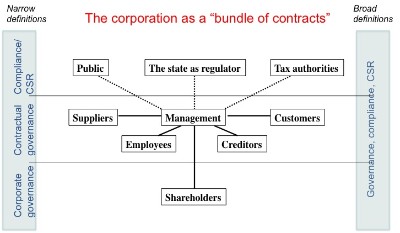

The corporation as a "bundle of contracts"

There are many perspectives or models for analysing business. For the purpose of corporate governance analysis, it is useful to view the corporation as a structure of stakeholder relations.

Relations with suppliers, employees, customers, creditors and shareholders are based on explicit agreements indicated by solid lines. The dotted relations with the state as regulator, tax authorities, or the public are not founded on bilateral agreements, but are nevertheless important as these stakeholders can strongly impact the business of a corporation.

Some people take a narrow perspective and confine corporate governance to the analysis of the shareholder-management relation, because of the special position of equity investors (see below) and the fact that other bilateral agreements are basically governed by contracts. They would further argue that the other relations belong to the realm of CSR and compliance. However, from a broader perspective, all stakeholder relations embody governance and compliance issues and can be subject to CSR considerations.

Shareholder versus stakeholder orientation

In a narrow sense, corporate governance is concerned with the protection of shareholder interests. The special attention paid to outside equity investors is due to their weak position. Unlike creditors, equity investors do not get their money back, and they have no contractual right to receive a certain income. They only have claims on the residual income, which means they get what is left after all the others have been paid, and this maybe less than nothing.

It is clear that management cannot afford to neglect any of the above stakeholder relations. In a competitive environment, profits can only be realised when all stakeholders are satisfied. Why then draw the distinction between "shareholder" versus "stakeholder" orientation?

Theoretically "shareholder orientation" means that the goal function of management is to maximize shareholder value subject to the constraint that all other interests are sufficiently served, whereas "stakeholder orientation" allows for other interests to directly enter the goal function.

The theoretical distinction abstracts from the real situation. From a pragmatic point of view one should assume that management has its own private goal function which it tries to maximize subject to the constraint of satsifying shareholders and other stakeholders.

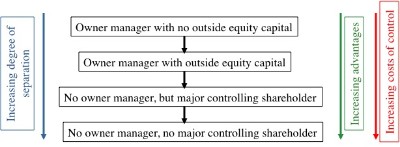

The separation of ownership and control

The weak position of outside equity investors explains, why most firms even in an advanced economy are run by owner managers. The costs of protecting the interests of outside equity investors would outweigh the benefit. However, in some instances the benefit seems large enough to afford the position of outside equity investors. Typical examples are

- highly capital intensive companies that need to raise huge sums of equity,

- high-tech start-ups that need to expand quickly to be successful, but bear a high risk of failing,

- second and higher generation family businesses, where at least some heirs do not participate in management.

A separation of ownership (provision of equity capital) from control (managing the company) has definite advantages. It allows for

- an investment of equity capital beyond the wealth of incumbent owner-managers,

- risk diversification - more investors can share in the risk,

- liquidity - outside equity investors cannot withdraw money, but they can trade their shares,

- specialisation in risk taking - let those with enough funds, expertise and risk taking spirit invest,

- specialisation in management - select the best, replace the unsuccessful.

The advantages weigh more the larger the company and the riskier its business is. However, realising them comes at a cost - outside equity investors need protection, and such protection cannot be easily provided as it cannot be arranged by simple contract.

The problems become more severe, the more the advantages of separating ownership from control are exploited. In the extreme case of fully dispersed ownership the advantages of risk diversification and liquidity are fully realised. At the same time, the control problem is most severe, because small minority shareholders neither have the information, nor the expertise, nor the incentive, nor the influence to control management. So how can it work? There are many solutions, but none of them is perfect (see here).